Federal Reserve Chair, Jerome Powell, was quite upbeat about recent economic data during a moderated conversation with the New York Times Dealbook. He noted that the since the Fed’s September meeting, growth has improved, while downside risks to the labor market have declined. At the same time inflation has come in a little higher. As a result, he believes the Fed can “afford to be a little cautious” on moving policy rates to neutral (the rate at which policy is neither stimulative nor restrictive). Other Fed members are also singing from the same hymnal, signaling a more gradual pace of normalization.

In my opinion, it’s very likely the Fed will cut rates by 0.25%-points at their December meeting (Dec 17th – 18th), taking the Fed funds rate to the 4.25 – 4.50 percent range. Fed funds futures are currently pricing in a 74% probability of a cut in December, and it’s notable that Powell didn’t say anything to push back on this. But the question is what happens in 2025.

2025 Cuts Are an Open Question

The Fed has two mandates — stable inflation and maximum employment. So when thinking about the path of rates, it’s best to think about what could happen in these two areas, especially relative to the Fed’s own projections (as outlined in their Summary of Economic Projections (SEP), which includes the “dot plot” for the fed funds rate).

Here’s what they projected in their September SEP:

- The unemployment rate at 4.4% for 2024 and 2025

- Core PCE (Personal Consumption Expenditures Index) inflation at 2.6% in 2024 and 2.2% in 2025

- Given the above two, they estimated the fed funds rate to be 4.4% for 2024 and 3.4% at the end of 2025

However, the data is upending the Fed’s projections. The unemployment rate is currently at 4.1%, below their 2024 projection of 4.4%. So, labor market risks are less of a worry now from their perspective. On the other hand, core PCE is on track to hit 2.8% in 2024, above the Fed’s projection of 2.6%.

The December rate cut seems very likely at this point, pulling the fed funds rate to 4.4%, which would be in line with their September projection for 2024. But this is in the face of both unemployment and inflation going in opposite directions from their forecast (unemployment below, and inflation above). That means they’re likely to shift their 2025 rate projection when they update the dot plot in December. The problem is that as we go into 2025, it’s very possible that the data continues to upend their projections. Unemployment could very well remain low (below 4.4%), assuming no labor market surprise. And inflation could stay “hot.”

Buckle Up, the Inflation Data Is a Mess

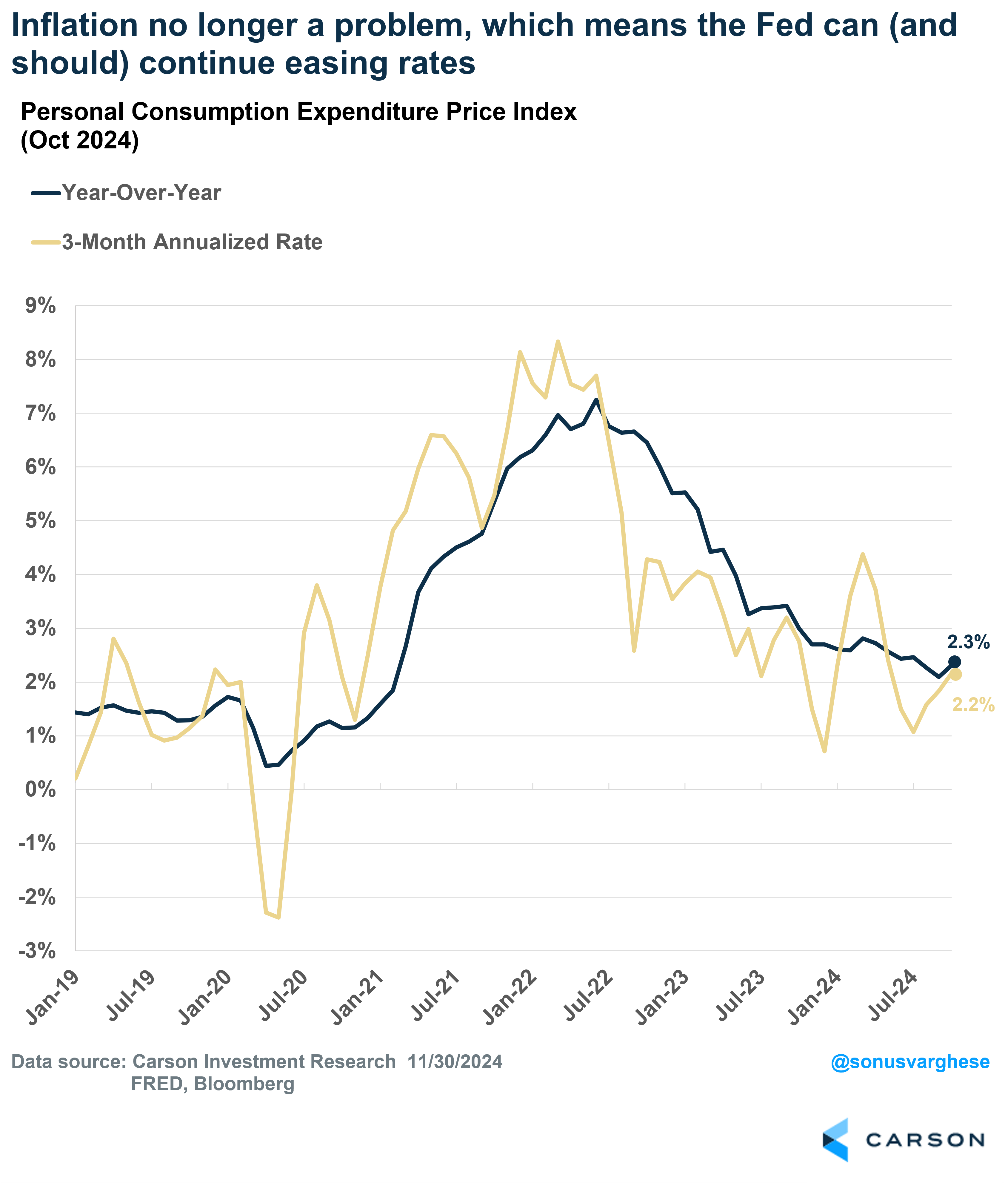

Headline PCE inflation currently shows no signs of concern, running at an annualized pace of 2.2% over the last three months and 2.3% year over year. As long as energy and food prices remain muted, headline inflation should be contained. Again, barring any surprises.

The Fed targets headline inflation, but they focus on core inflation as a gauge of underlying inflation and a rough forecast of where headline inflation may go. The problem is that the core PCE data are a mess, and for the matter core CPI too (Consumer Price Index). Core PCE is up 2.8% over the last three months (annualized) and year over year. But that 0.80%-point overshoot versus the Fed’s target of 2% is not really capturing underlying real-time inflation. Instead, about 0.63%-points of that overshoot is coming from two sources, housing and financial services.

The Fed targets headline inflation, but they focus on core inflation as a gauge of underlying inflation and a rough forecast of where headline inflation may go. The problem is that the core PCE data are a mess, and for the matter core CPI too (Consumer Price Index). Core PCE is up 2.8% over the last three months (annualized) and year over year. But that 0.80%-point overshoot versus the Fed’s target of 2% is not really capturing underlying real-time inflation. Instead, about 0.63%-points of that overshoot is coming from two sources, housing and financial services.

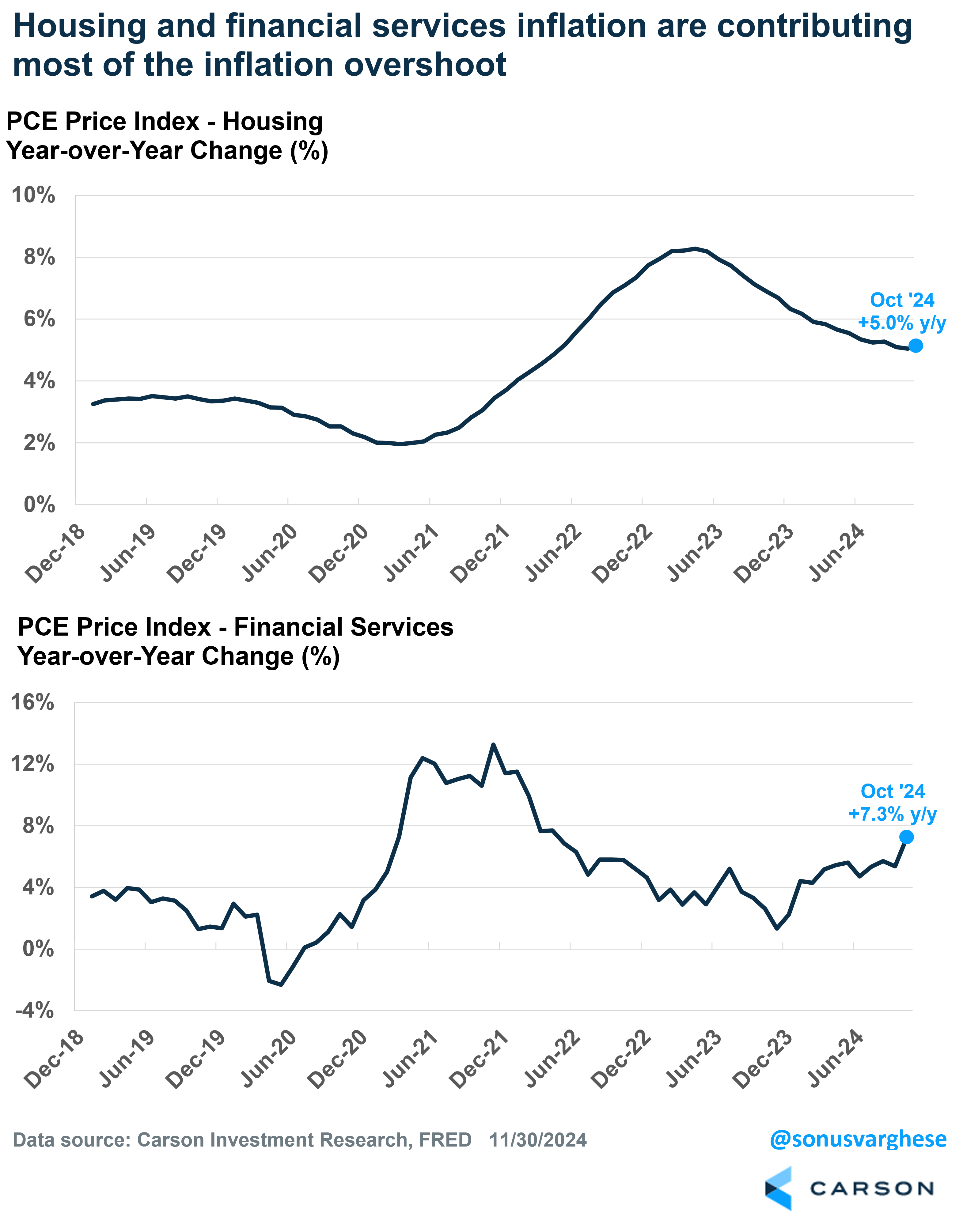

We’ve discussed a lot about how housing inflation is really capturing lagged dynamics of what happened in 2021 and early 2022, as opposed to what’s happening real time. The good news is that we’re seeing housing disinflation, and there should be more in the pipeline for 2025. The bad news is that it’s happening slowly. Housing inflation (which makes up 17% of the core PCE basket) is up 5% year over year, down from 6.3% at the end of 2023 and 7.7% at the end of 2022. But we still have some ways to go to hit the pre-pandemic pace of about 3.4%.

Financial services make up just under 10% of the core PCE basket. And right now, it’s elevated because of surging stock prices, which is driving portfolio management services inflation higher. Also, the spread between what banks pay all of us on deposit accounts versus the fed funds rate is large right now, and this shows up as “inflation” in the government data. It does become less of a problem as the Fed lowers rates, but for now it’s contributing more than it did pre-pandemic. The PCE index for financial services is up 7.3% year over year, the fastest pace since March 2022. Contrast that to a 1.3% pace in December 2019.

It would be one thing if housing and financial services inflation were reflecting a real-time inflation dynamic. But that’s clearly not the case. As I noted above, housing inflation is severely lagging private market data, and financial services is imputed from market prices. I don’t think any of us will complain about surging stock prices and would not root for the opposite (never mind the bears).

The problem is that neither of these dynamics is likely to fully abate in the first part of 2025. Housing inflation may remain elevated for a while longer, even as it continues to pull lower ever so slowly. The Q4 surge in stock prices could likely keep financial services elevated as well. On top of that, seasonal adjustments since the pandemic have been messy and residual seasonality could likely result in elevated inflation data in Q1 (we saw this at the beginning of this year). Moreover, we could very well see less disinflation in commodities outside food and energy (like used cars, apparel furnishings, and appliances).

All this means core inflation could stay elevated through the first quarter of 2025, and perhaps through the first half, clocking in well above the Fed’s 2025 core PCE projection of 2.2%. That could very well keep the Fed on pause in early 2025. Of course, this assumes we don’t get a big downside surprise on the labor market side, but that’s not something we want to root for (bad news will be bad news in our book).

Forward Looking Measures of Inflation Don’t Show a Problem

In contrast to the backward-looking data, forward looking measures show that inflation has mostly normalized.

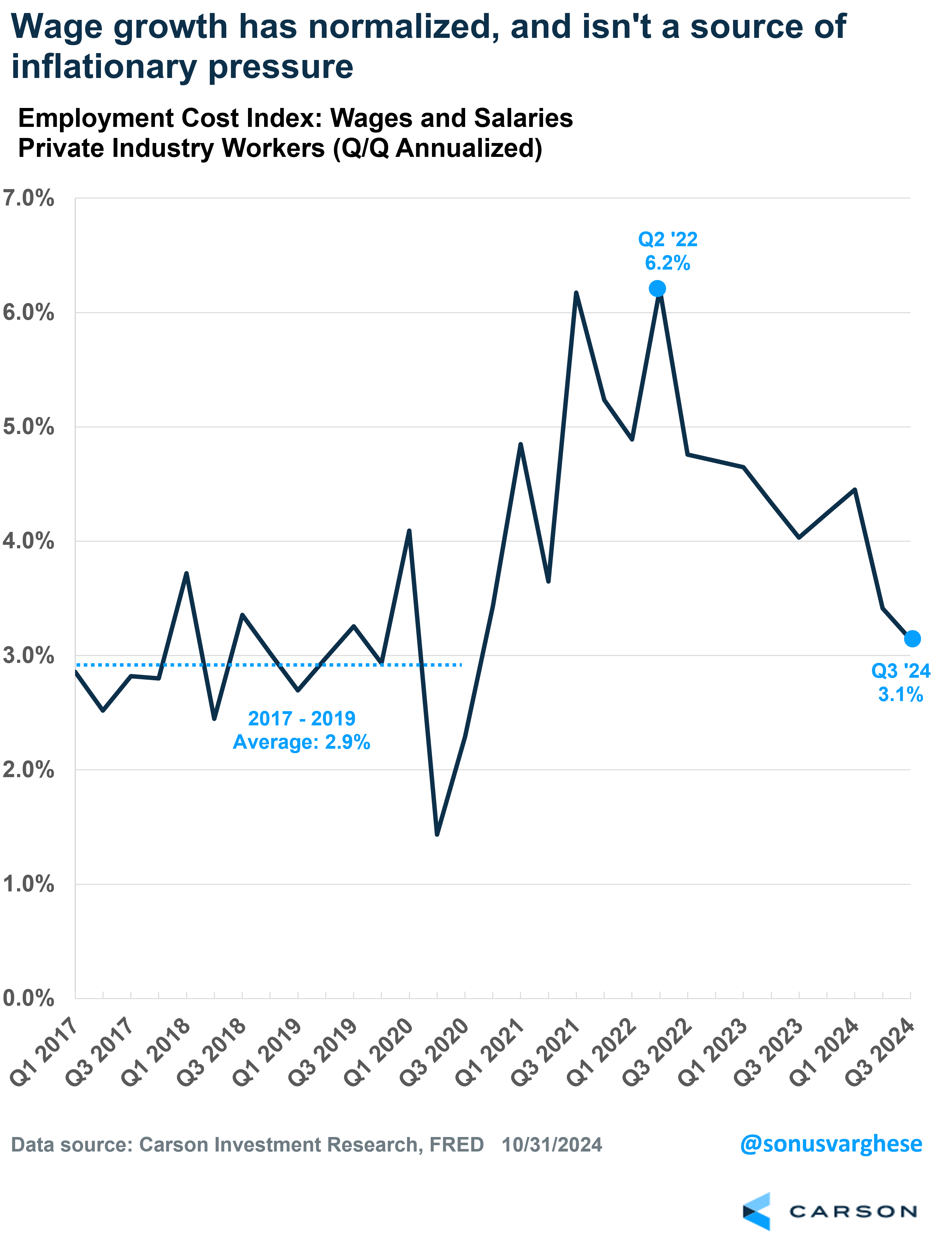

One, wage growth has eased a lot. The Employment Cost Index (ECI), which is the gold standard of wage growth measures, was up 3.1% (annualized) in Q3 2024. That’s still solid, but consistent with 2% inflation. The pre-pandemic pace was 2.9% for comparison. In fact, Powell himself noted recently that the labor market is no longer a source of inflationary pressure. (My question is, then why not normalize rates sooner rather than later?)

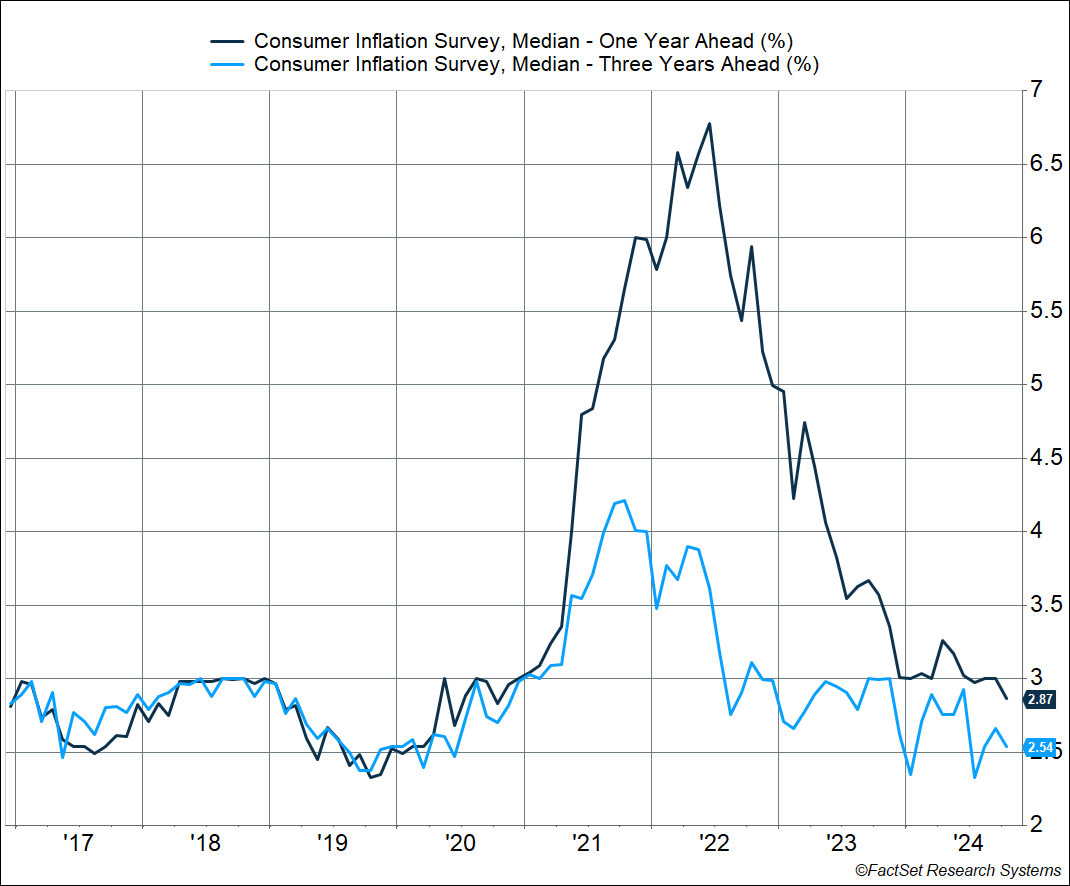

Two, consumer expectations of inflation have also normalized. The New York Fed’s consumer survey showed that 1-year ahead inflation expectations are at 2.9% and 3-year ahead at 2.5%. These are consistent with what we saw pre-pandemic, when overall inflation was muted. Moreover, consumers tend to project current inflation into the future. The fact that current expectations match what we saw in the 2017-2019 period suggests inflation has normalized.

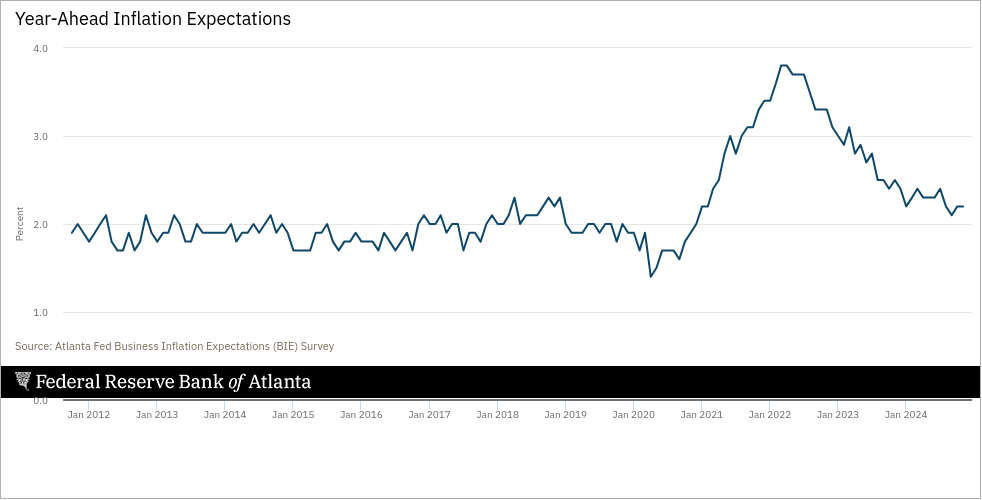

Three, business expectations of inflation have mostly normalized. The Atlanta Fed’s survey of businesses found that 1-year ahead inflation expectations are at 2.2%, not far above the 2017 – 2019 average of 2%.

Keep in mind that inflation (at least measured by core PCE) was running below the Fed’s target of 2% before the pandemic. The fact that all the three measures I discussed above are close to pre-pandemic levels suggest underlying inflation is close to 2%.

Ultimately, if the Fed does pause for an extended period of time, that’s going to be on the back of spurious, backward-looking inflation data, rather than what’s happening in reality, let alone forward-looking measures like wage growth and inflation expectations. Meanwhile, policy would implicitly be getting tighter, as policy rates stay elevated and underlying inflation remains muted. That’s a big risk for cyclical sectors of the economy, like housing and even manufacturing and business investment.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

I still think we could see 2-3 rate cuts in 2025 (each worth 0.25% points), but we may have to sit on our hands a bit before that comes to pass. Even if we don’t see that many rate cuts in 2025 (or none), it’s likely not going to pull the economy into a recession next year, in my opinion. But it’s not a good scenario for growth prospects, let alone an equity market that may be banking on rate normalization. Chief Market Strategist Ryan Detrick was out this week for our Facts vs feelings recording, but VP, Asset Allocation Strategist Barry Gilbert and I discussed a lot of this stuff in our latest episode. Take a listen.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

02538931-1224-A