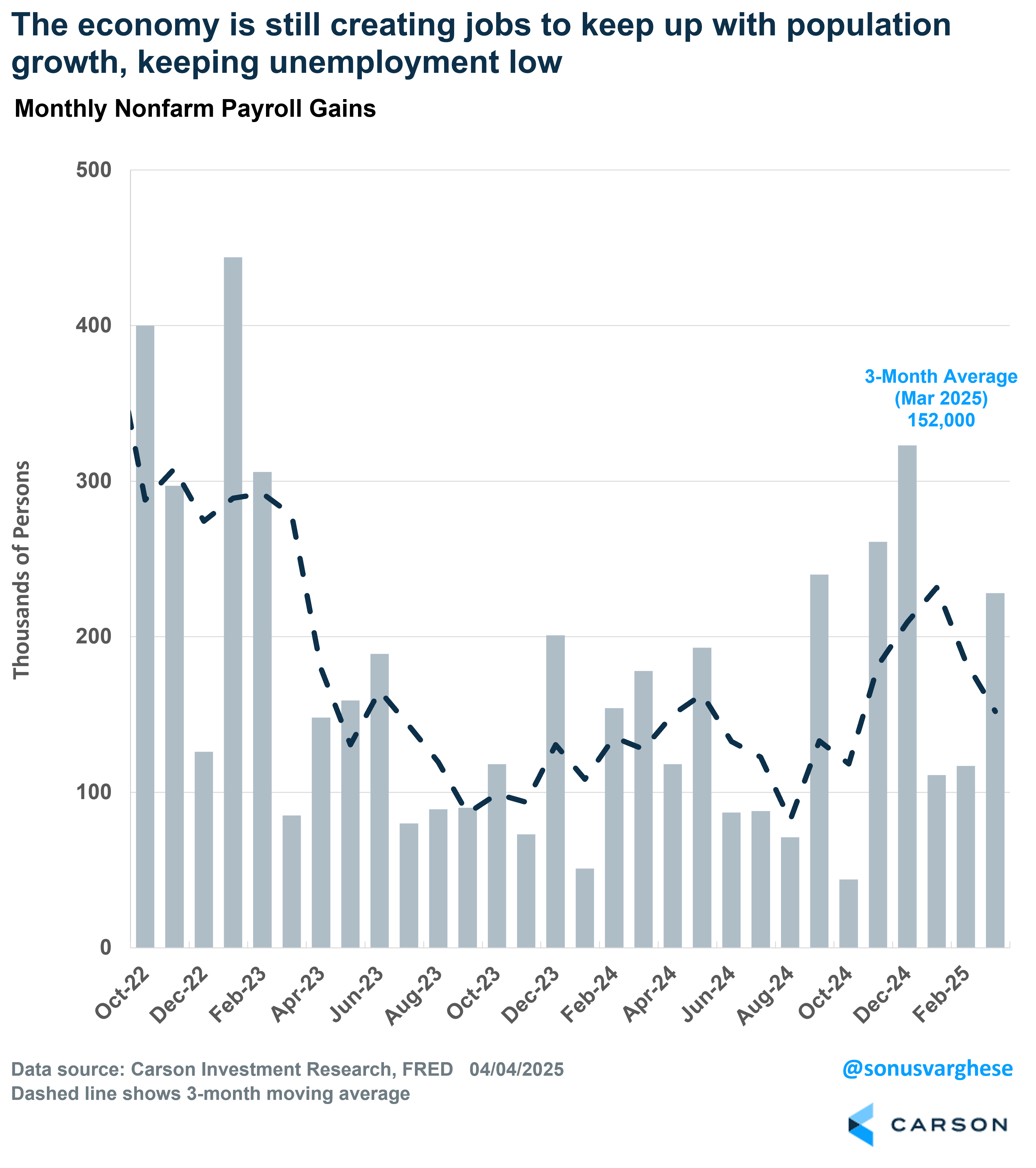

The economy created 228,000 jobs in May, well above the 140,000 that was expected by forecasters. Monthly numbers can be noisy (especially since some of the jobs created could be a rebound from lower-than-expected numbers after terrible weather January and February) and so let’s look at the three-month average. That’s running at 152,000, which should be more than enough to keep up with population growth, especially in the face of a big drop in immigration. Of course, that’s lower than the monthly average of 209,000 in the fourth quarter of 2024—so the labor market has certainly cooled.

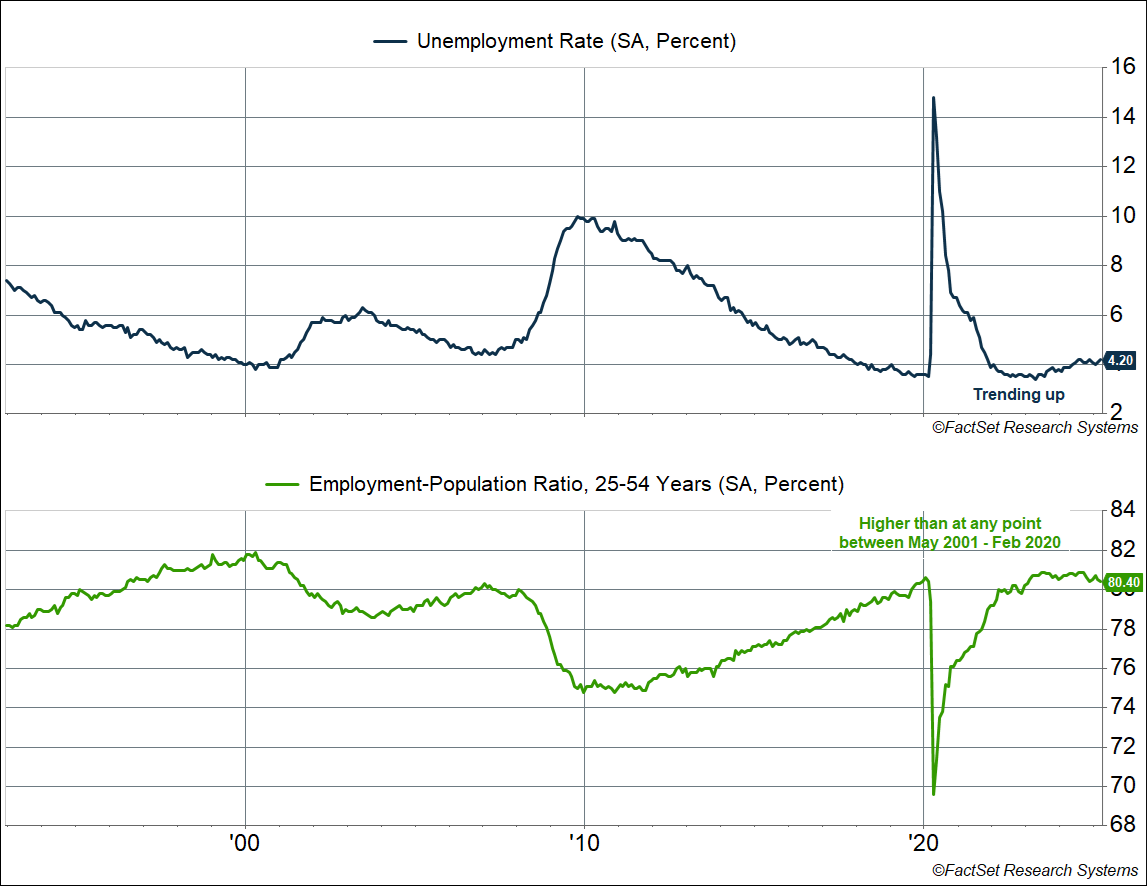

The unemployment rate did tick up from 4.1% to 4.2%, but that’s a result of rounding. It actually moved from 4.14% to 4.15%. Let’s call that steady. The prime-age (25-54) employment population ratio, which I prefer to the unemployment rate since it gets around demographics (an aging population) and definitional issues around who is counted as “unemployed,” is now at 80.4%. That’s dropped from a peak of 80.9% last September. That’s concerning by itself, and more evidence that the labor market is cooling. At the same time, 80.4% matches the highest levels we saw between 2001 and February 2020, implying the labor market is still in an “ok” place overall (as long as the numbers don’t move lower). Note that this also means we don’t’ have a lot of workers “sitting on the sidelines” that can be employed to build all the new manufacturing facilities that will need to be reshored to America, let alone workers to make goods in them.

What ultimately matters for the economy is aggregate income growth, because that will determine how much capacity there is for spending. It’s a gauge of the speed limit of nominal GDP growth. Aggregate income growth is the product of:

- Employment growth, which is fairly solid at 1.3% year over year, but lower than the 1.5% pace we saw in 2019

- Wage growth, which is running at a 4.2% year-over-year pace, ahead of the 2019 run-rate of 3.4%

- Hours worked, which is where we were pre-pandemic

Aggregate income growth is up 4.4% year over year as of March 2025, and the three-month annualized pace is actually 4.9%. That’s in-line with the pre-pandemic pace of 4.5%.

This is all positive news, but it’s yesterday’s data. It tells you that the economy was in a reasonably good place going into a massive shock event, i.e. tariffs. It’s really hard to say what happens next.

As I wrote yesterday, the easiest way to think about tariffs is that it’s a tax increase for consumers and businesses—a big tax increase given the size of the tax cuts. The tariffs are going to create enormous distortion in consumption, and even investment data, over the next few months and we’re not going to be able to get a proper read on the economy. Meanwhile, we’re likely to see inflation data start to pick up after April and May, especially for durable goods like vehicles, as consumers rush to get ahead of tariffs. Businesses may also look to build up inventory at current low prices, which may result in a temporary boost in production. All this to say, the economic data over the next few months may be screwy and even likely to hide underlying weakness.

We’re also going into earnings season soon, but Q1 earnings are not going to mean much anymore, and I’m hard-pressed to think if a lot of companies are willing to give much guidance. At best, they’ll say they can weather the coming storm, but of course they’ll do that to avoid investors panicking and selling their shares.

The Economy Needs Support That Is Not Forthcoming

The president and his team are actively engaging in policy that is seeking to break how the global economy works, and re-tool it for long-term gain. But as I wrote in my prior blog, I’m unconvinced on the long-term gain part because of incompatible goals: generating more revenue for the US government versus re-shoring manufacturing versus liberalizing trade even further (as other countries drop all trade barriers). The way the tariff policy was constructed also leaves less room for negotiation. A country like South Korea already has near zero tariffs on US goods, and so what would the have to offer in a negotiation?

Congress is on the sidelines. Technically, tariff policy needs to be signed off by Congress, but that power has been eroded since the 1970s and ceded to the executive. They could buffer the blow to the economy with a fiscal package but right now the focus is simply on extending the tax cuts that are expiring at the end of this year. That’s positive, but all it does is remove another potential headwind, rather than adding a tailwind. If anything, Congress seems actively looking at options, including raising top tax rates, to avoid raising the deficit any further, a worthwhile long-term goal but not positive in terms of providing short-term support for the economy.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

That leaves the Federal Reserve (Fed). As I mentioned above, inflation is likely to pick up on the back of higher prices for durable goods—both because consumers’ rush to get ahead of tariffs, and subsequently as a result of a tariffs themselves, assuming businesses chose to pass along higher input costs instead of reducing their margins. In theory, the tariff impact will be “transitory,” a one-time shift in the price level. But because of how households may adjust spending, how companies choose to raise prices and revise contracts, and how inflation data is constructed, we may actually see persistently higher inflation for a period of time, beyond just 3 – 4 months. For example, we could initially see new vehicle prices go up as consumers rush to buy, followed by a spike in used car prices as people avoid tariffed new vehicles, followed by increased auto-service costs including maintenance and repair, and insurance.

It’s going to be a big problem for the Fed, and Fed Chair Jerome Powell acknowledged as much on Friday morning. He said that that while uncertainty is elevated, it’s now clear that the tariff increases will be significantly larger than expected. He seemed less convinced that the impact will be transitory, saying:

“While tariffs are highly likely to generate at least a temporary rise in inflation, it is also possible that the effects could be more persistent.”

He added that they will be focused on making sure that a one-time increase in the price level does not become an ongoing problem.

Over the last year, the Fed had decidedly moved policy to favor an asymmetric response to employment vs inflation (their two mandates). With the inflation outlook looking stable, they could focus on protecting the labor market, which is why they dropped rates by 1%-point last year to preempt weakness in the labor market (the unemployment rate rose from 3.7% in January 2024 to 4.2% by August). But that asymmetry may be ending, more so because the labor market doesn’t look like it’s breaking down (yet), even as inflation is likely headed in the wrong direction.

In fact, Powell’s remarks sound like a central banker who is once again considering the option of raising rates to fight inflation. I don’t think the Fed will raise rates this year, but even if they don’t cut, that still leaves rates in meaningfully restrictive territory (using their own terminology to describe where policy is). That’s going to hurt the labor market, along with cyclical areas of the market like housing and manufacturing.

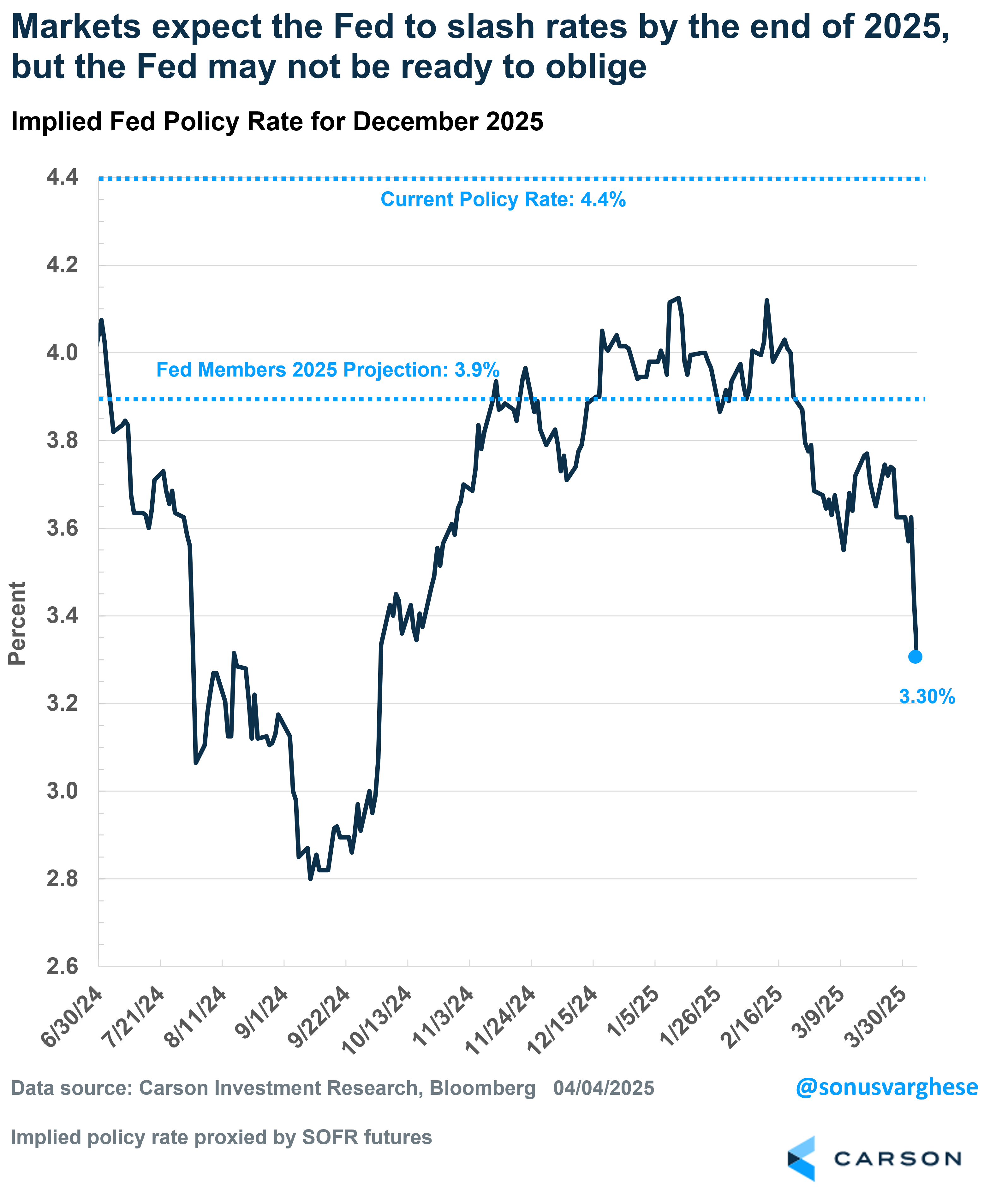

Interestingly, investors expect the Fed to cut policy rates all the way down to 3.3% by the end of 2025, 1.1%-points below where rates are currently (implying 4-5 cuts). Plus, they expect these cuts to come after the June Fed meeting. This means investors expect the Fed to slash rates in the back half of the year. Let’s be clear, it’s the market’s equivalent of thinking there will be a recession, with a big jump in the unemployment rate that the Fed will have no option but to respond to.

I don’t think it’s as clear cut as that. Core inflation could be headed back to 3.5% (it’s at 2.8% now, uncomfortably above the Fed’s 2% target) and it’s not a certainty that the labor market will collapse. We’re not seeing any signs of that, yet. In their March “dot plot,” Fed members expected the 2025 policy rate to end up at 3.9% (implying two cuts), with core inflation at 2.8% and the unemployment rate at 4.4%. It’ll be interesting to see where they put the dots at the next update in June. My guess is the projected rate for 2025 goes up, and projected core inflation and projected unemployment rate also goes up. That will not be positive for markets.

To summarize where we are as the economy faces a massive shock:

- The administration’s policies are actively looking to break how the global economy works, to retool for long-term gain (a very hard project to accomplish).

- The Fed is on the sidelines as they wait for data, and will likely only act after the labor market is breaking, and worse, they may even consider rate hikes if inflation stays persistent.

- Congress is on the sidelines, with no prospect of providing fiscal support. At best they extend the tax cuts, and that simply removes a headwind rather than providing a tailwind.

- Markets have significant concentration risk (towards the technology sector) and elevated valuations, which simply means there’s room for a bigger re-rating of expectations.

- The good news is that consumers and businesses are not leveraged to the hilt, but that lowers the odds of a big financial crisis, not the odds of a downturn spurred by retrenching.

Expect turbulence ahead. This is the time to have portfolios diversified as much as possible, without leaning too much one way or the other. Of course, markets pulling back is an opportunity to add more at lower prices, especially if you’re invested for the long term. But the long term is a series of short-term windows and you need to be sure that your risk allocation matches your tolerance for volatility, as we could see a lot of it in the months ahead.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7823260.1-0425-A