The October Consumer Price Index (CPI) data held no surprises for markets, either to the downside or the upside. Since inflation had already normalized, that means the latest data confirms the pre-existing trend. Headline CPI rose 0.2% in October and is up 2.6% year over year. Core CPI (excluding food and energy), which is typically used as a gauge for underlying inflationary pressure by the Federal Reserve (Fed), rose 0.3% last month and is up 3.3% since last year.

It probably sounds bonkers to say inflation has normalized when these numbers are clearly above the Fed’s target of 2%. The thing is, almost all of the “excess” inflation is coming from shelter inflation. If you take out shelter inflation, which makes up about 35% of the CPI basket, headline CPI is up just 1.3% year over year. Even over the last three months, CPI ex shelter is running at an annualized pace of 1.3% versus 2.5% for overall CPI.

You may be thinking, “Wait! Housing is in fact a big portion of a household’s budget. You can’t just throw it out.” That is true, except the heat in shelter inflation actually comes from rent increases we saw in 2021, when rents surged. As Ryan and I have discussed over the last two years, official shelter data has significant lags to what we see in the private market real-time data. Private data (via Apartment List) indicates that rental inflation has slowed significantly, and new rental lease prices have been falling for over a year now. Our friends at WisdomTree have done one better, re-constructing CPI, but with more real-time housing price data. This is from their data:

- Headline CPI with real-time shelter is up 1.3% year over year versus 2.6% for CPI with official shelter data.

- Core CPI with real-time shelter is up 1.8% year over year versus 3.3% for core CPI with official shelter data.

Jeremy Schwartz, the Global Chief Investment Officer at WisdomTree, put it succinctly: “The Fed should continue recalibrating to neutral.” I couldn’t agree more.

The good news is that the Powell-led Fed seems inclined to do so as well. There’s been a question about whether the Fed should be cutting when economic growth and the stock market are running strong. But the Fed does not have a GDP mandate. Nor do they have a stock market mandate. As Ryan pointed out in his last blog, the Fed has historically cut with stocks near all-time highs (and stocks were higher 20 out of 20 such times a year later, with an average return of 14%). The Fed has a stable inflation mandate, and a maximum employment mandate. It’s pretty clear the former goal has been met. But there’s some risk to the latter, which the Fed seems thankfully aware of. As Powell said after the most recent Fed meeting in November:

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

“The labor market has cooled a great deal from its overheated state of two years ago and is now essentially in balance. It is continuing to cool, albeit at a modest rate, and we don’t need further cooling, we don’t think, to achieve our inflation mandate.”

In short, the Fed doesn’t want the labor market to get weaker. Their most recent unemployment rate projections (from the September meeting) confirm this – they projected the 2024 and 2025 unemployment rate to remain steady at 4.4% (it’s currently at 4.1%). As I wrote back then, the Fed is essentially putting a cap on the unemployment rate, or rather, a floor under the economy. Crucially, the fact that inflation has normalized is what allows them to do this. There’s good reason to think this dynamic will play out in 2025 as well, with shelter disinflation in the pipeline and continuing to put downward pressure on overall inflation.

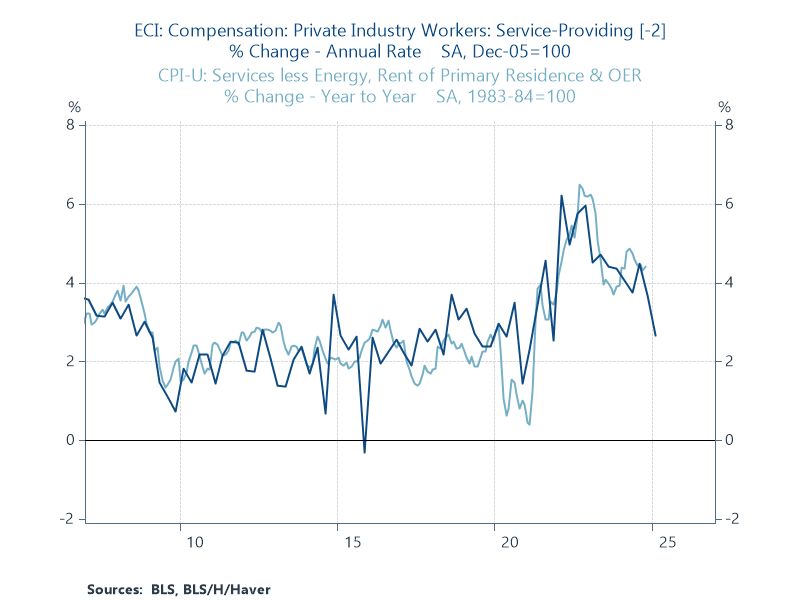

To Powell’s point, the labor market does not need to cool further for them to achieve their inflation mandate. And it had cooled quite a bit, as Neil Dutta at Renaissance Macro Research points out. A good place to see this is in wage growth. The latest Employment Cost Index data for private sector service industry workers showed wages growing 3.6% since last year but slowing to a 2.7% annualized pace in Q3. This metric is historically correlated with services inflation, and it looks like there’s further moderation ahead.

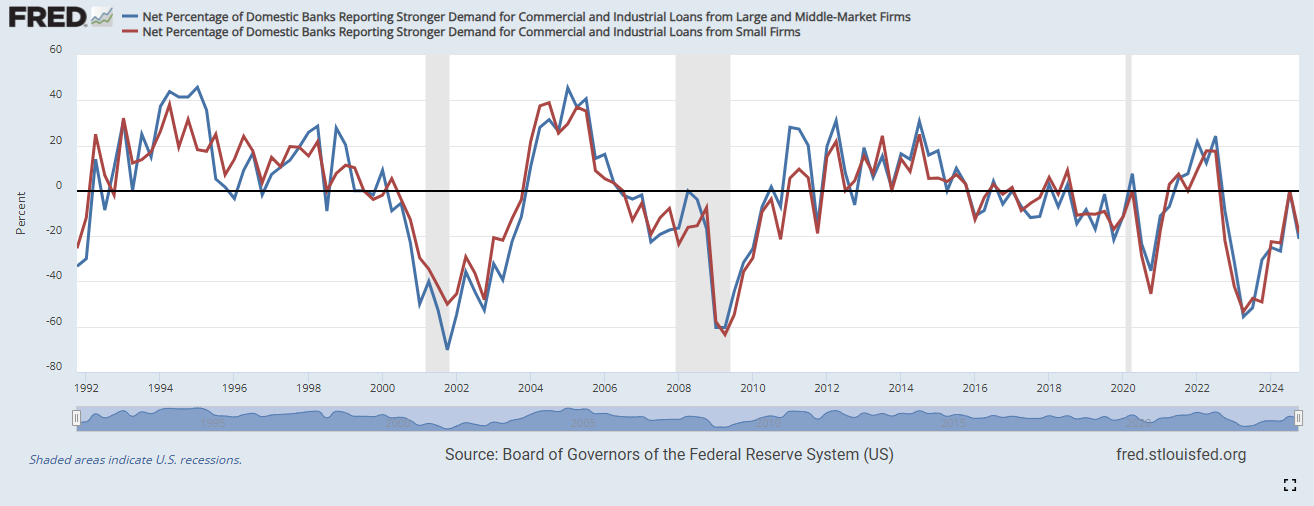

This is further confirmation that the inflation problem is over, and the Fed can normalize interest rates (and should do so). Elevated rates are clearly having a negative impact on rate-sensitive segments of the economy, especially housing. The Fed’s latest survey of bank loan officers also showed much weaker demand for loans in Q3, despite a pullback in the net number of banks tightening standards. The net percent of banks reporting stronger demand for commercial and industrial loans pulled back from 0% to -21% for large and middle-market firms, and from 0% to -19% for small firms. This is not what you want to see if investment spending is to pick up.

Long story short, policy is too tight. But the Fed has a lot of room to cut because inflation has normalized, and the inflation outlook looks good as well.

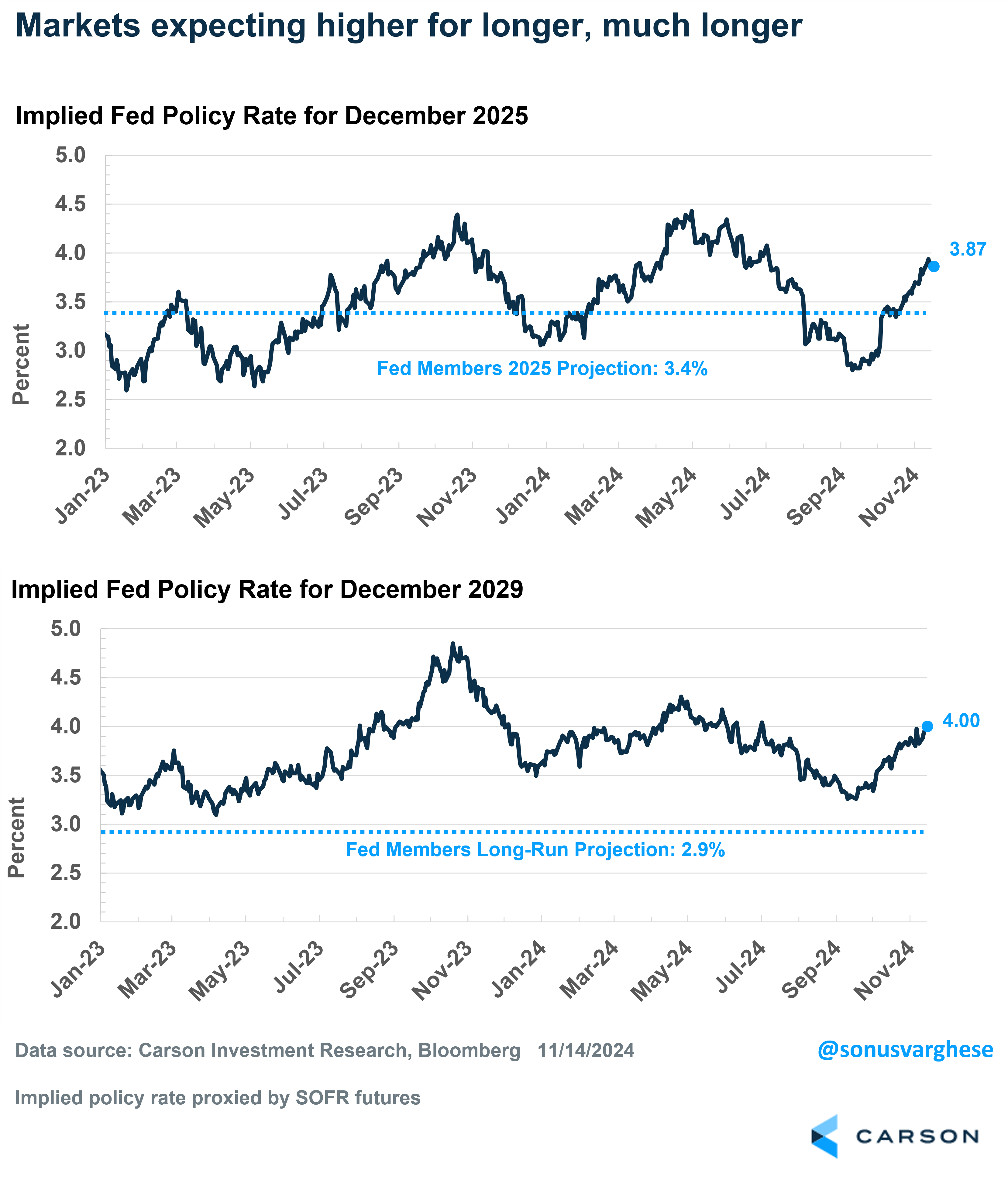

What’s interesting is that markets are now more hawkish than the median Fed member. Markets currently expect the policy rate to land around 3.9% at the end of 2025, implying just 2-3 more rate cuts. Fed members estimated the 2025 rate at 3.4% in their September projections. Looking further out into 2029, markets expect the policy rate to remain close to 4%. That’s well above the Fed’s long-run estimate of just 2.9%. At some point these divergent views will have to reconcile, and it may take investors becoming a tad less optimistic about future growth and perhaps Fed members becoming a tad more optimistic.

Ryan and I talked about the post-election market moves and economic picture in our latest Facts vs Feelings podcast episode. Take a listen below.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

02508771-1124-A